We are delighted to inform our clients on the accessibility of trading stock CFDs starting April 10, 2018, Tuesday. This exclusive asset class is our latest additional offering among others that will soon be available on our MT5 platform.

Exclusive Change Capital, as an Investment Firm incorporated under the laws of Cyprus with registration number: HE 337858, proudly announces the acquisition of its license number CIF 330/17.

Our company proudly announces the acquisition of its Portfolio Management licence as of April 16, 2018. This licence endeavours our ongoing attempts in the provision of quality and high-ended services in a wider spectrum.

Exclusive Capital is delighted to announce that Marshall Gittler, Chief Investment Strategist for ACLS Global, will be consulting with our portfolio investment team and contributing his FX commentary to our website. Mr. Gittler is well known as a strategist, investment specialist, and economist, with decades of experience working for the major investment banks in Europe and Asia.

Exclusive Change Capital Ltd. is pleased to announce that it has received the International Quality Certification ELOT EN ISO 9001:2015. This certification is addressed to organizations that wish to ensure their ability to provide products and services that meet customer requirements and comply with the legal framework.

We would like to congratulate the young Cypriot athlete Petros Englezoudis on having a great athletic year and becoming a Youth Champion in Skeet Shooting 2019.

As the latest situation in the Middle East has become one of the most recently discussed topics, our Head of Investment Research Vrasidas Neofytou will analyse the geopolitical developments on RIK1 TV program «Απο Μερα σε Μερα» on Wednesday, September 18th at 12:20 pm.

Since 2012 the Finance Magnates’ London Summit has been the leading event for professionals within the financial industry.It is a superb meeting place for finance-oriented individuals, entities, and organizations, such as liquidity providers, marketing specialists, brokers, and banks for educational and networking purposes.

It was our pleasure to be a part of three magical evenings in Episkopi Village, Limassol supporting the charity Christmas Village activities which took place from the 20th till 22nd of December, 2019.

Following a great effort from Exclusive Capital's management team to reduce smoking among employees during 2019, the company`s directors have decided to grant additional 5 days paid annual leave as a reward to those employees who make an effort not to smoke or to quit smoking.

Take advantage of an institutional infrastructure while remaining at the forefront of the latest financial market developments. Our reputation will ensure that you exceed your client’s expectations for service, pricing, and security.

At Exclusive Capital our portfolio management team is carefully selected based on sophisticated knowledge and vast experience. Our capabilities offer robust portfolio management services.

Exclusive Capital takes an innovative approach in delivering returns by utilizing investment strategies in private equity, venture capital, tangible assets, and extensive alternatives.

We provide an exceptional trading experience utilizing cutting edge technology with highly competitive spreads. If you are looking for an investment proposition that best matches your needs, we have the tools to help.

We have developed an in-depth understanding of the intricacies of wealth to deliver insightful and effective advice for investment. Our investment process is characterized by rigor and discipline and is reflected through the quality of our work.

The US dollar ends 2020 in a downtrend momentum against major currencies as investors move away from the safety of the greenback, betting on the global economic recovery in 2021 and the continued US fiscal and monetary policies.

The DXY-dollar index against a basket of six major currencies stood at 89.60 on Thursday, having hit its lowest since April 2018. The Euro trades near $1.23 while Pound Sterling advances near $1.3650, hitting their highest levels in 2.5 years against the US dollar, gaining support after Britain and European Union reached a post-Brexit trade deal agreement on Dec.24.

Furthermore, the Euro currency receives more demand vs dollar, since the Eurozone economy runs a huge current account surplus, thanks to exports of Germany and other industrial EU countries, while the US economy has a 12-year record current account deficit which causes further weakness to US dollar.

EUR/USD pair, Daily chart

The greenback’s devaluation continued this week after the US President Donald Trump signed the well-expected $900 billion coronavirus aid package and spending bill on Sunday, to help reduce the damage of the pandemic in the world’s largest economy.

The fresh US stimulus bills are dollar-negative catalysts since they grow the nation’s budget deficit, increase the inflationary pressure in the economy (higher commodity prices), resulting in a real dilution of greenback’s purchasing value.

Safe havens under pressure:

The “safe-haven” currencies US dollar, Japanese Yen, and Swiss Franc have been under pressure against riskier currencies such as the Euro, Pound Sterling, and the dollars of Canada, Australia, and New Zealand in the second half of 2020.

The combination of massive fiscal and monetary policies around the world, the approval of the US stimulus bill, the start of mass vaccination programs in Europe and the USA, the relief over the well-awaited Brexit deal have bolstered risk appetite sentiment and created a positive backdrop for riskier currencies and global equities going into 2021.

The trade-sensitive Canadian, Australian, New Zealand dollars, and Asian currencies have climbed to the highest level in 2 years against the greenback amid the hopes that the rollout of Covid vaccines would end the widespread lockdowns and bring an economic normalisation next year.

Hence, the commodity-sensitive Mexican Peso, Norwegian Krone, and Russian Rubble hit yearly highs against the US dollar amid the tremendous rally in the commodity sector led by Crude oil and industrial metals (Copper, Iron Ore).

The trade & commodity-sensitive currencies are considered barometers of the risk appetite sentiment among market participants because of their trade ties with China and global commerce.

2021 US dollar Outlook:

The weaker demand for the US dollar is expected to remain in 2021 if the Federal Reserve keeps its loose monetary policy and interest rates near zero. Also, the new elected President Joe Biden is expected to push more economic support measures (extends current fiscal packages) since the second wave of pandemic and the resumption of social restrictions have become a real threat to the US economy.

Global equities rallied strongly at the start of the final trading week of 2020, as investors celebrate the Brexit trade agreement, the start of vaccinations in Europe, the positive news over AstraZeneca’s vaccine and the signing of the well-expected US Covid-19 relief package by President Trump.

US stimulus relief package:

Appetite for riskier assets increased this week after US. President Donald Trump signed a $900 billion coronavirus relief package into law on Sunday. Trump prevented a government shutdown late Sunday, extending the unemployment benefits into March for an estimated 14 million people in the USA. The new package includes a $600 direct payment to most individuals and adds $600 for every child.

President Trump suggested last week to veto the legislation demanding $2,000 direct payments instead of $600. The House voted Monday to increase the second round of federal direct payments to $2,000, leaving it up to the GOP-controlled Senate.

The stimulus-led market euphoria sent the industrial Dow Jones to close at fresh record highs of 30.400, up 0.7%, while S&P 500 and Nasdaq finished on Monday higher by 0.9% to 3.735 points and 0.7% to 12.900 points respectively, reaching new all-time highs as well.

Dow Jones index, Daily chart

Dow Jones and S&P 500 gained 6% and 15% respectively in 2020 recovering all Covid-led losses. However, it was the technology-focus Nasdaq Composite that outperformed the whole market, adding more than 45% in the same period as investors felt safe to position their funds into pandemic-winner tech names such as Netflix, Amazon, Zoom, and Apple.

Brexit trade deal and AstraZeneca’s vaccine:

Germany’s DAX index finished up 1.5% on Monday, erasing almost all pandemic-led losses, while France’s CAC rose 1.3%, on Brexit deal optimism, AstraZeneca vaccine news, and the start of mass vaccinations in Europe.

Britain’s FTSE 100 hit 8-month highs at 6.660 points on Tuesday after the drug maker AstraZeneca announced that its COVID-19 vaccine candidate is set to be granted emergency use approval from UK regulators this week. Hence, the company believes that its vaccine would be effective against a new variant of the virus that has helped drive a spike in cases in Britain.

European investors also cheered the long-awaited Brexit trade deal between the European Union and Britain last week. Euro and Pound Sterling currencies rose to 2 ½ year highs against the US dollar.

Asian Markets:

Equities in Asia were higher this morning, following the overnight gains on Wall Street. The Japanese index Nikkei 225 finished Tuesday’s session with 2% gains at 27.560 points, trading at levels not seen since 1990. South Korea’s Kospi finished the day at 2.820 points, up 0.50%, hitting fresh all-time highs, the Hang Seng gained 1% near yearly highs, while Australia’s ASX 200 rose 0.50%.

Crude oil gains:

Crude oil rose on Tuesday along with gains in global equities, over the growing optimism that the fresh US stimulus bill combined with the expectation for a global economic recovery in 2021 would increase the demand for petroleum products.

WTI and Brent crude prices added 1% yesterday, to $48 and $51 per barrel respectively erasing most of last week’s losses propelled from concerns over the new fast-spreading Covid variant in the UK.

Market outlook for 2021:

The market outlook for 2021 will remain bullish if the pandemic-damaged global economies will be supported by the ongoing massive monetary and fiscal stimulus, the low-interest rates, the weaker US dollar, and the successful mass vaccination of the global population which will allow economies to reopen after the devastating COVID-19 pandemic.

The UK assets opened the week with significant losses on concerns over a fast-spreading coronavirus strain in the country and little progress on a post-Brexit trade deal.

The FTSE 100 Index tumbled as much as 3% on Monday as UK travel, airline, and retail shares were among the worst hit. Pound Sterling lost more than 2% against major currencies, the biggest drop since October, as investors moved to more safe-haven currencies.

The new variant that emerged in southeast England in September, is causing concerns as it is reported to be as 70% more transmissible than other strains and may be contributing to a spike in cases in the country, However, health experts said that Pfizer’s and Moderna’s vaccines would likely be effective against the new variant.

Prime Minister Boris Johnson announced emergency lockdowns in London and other regions over Christmas to curb the spread of the new strain, while several countries banned flights and suspended rail links with the UK.

The uncertainty about the new variant, together with the resumed lockdowns and travel bans have dampened the mood for UK economic prospects, as there is a growing fear that the virus situation will remain on course at least through Q1 2021.

We all know economies will experience a burst of growth with the introduction of a COVID vaccine that will hopefully lead to an end of the current pandemic. Part of the growth will come from pent-up demand, part from increased productivity (gained during the pandemic), and lastly growth due to the return of sectors like hospitality, which are almost non-existent today. However, with 93% of economies around the world locked down and struggling from the pandemic, it’s hard to make a case for a return to pre-COVID normality anytime soon.

Assessing economic growth and trying to predict what markets will do in 2021 is a great challenge, because many of the implications of the 2020 crisis have yet to manifest themselves. Not only are the long-term health repercussions of the pandemic still unknow, but there are many questions pertaining to the state of small businesses, hospitality, and a host of other sectors that have been affected by the pandemic.

Furthermore, unemployment is still a concern. The outlook for the labor market in Europe is of particular concern. Increased unemployment and increased long term unemployment are issues central bank liquidity cannot address.

We have all noticed the divergence between economic activity and market performance. Many (myself included) have wondered why. One explanation is that the liquidity created by central banks has increased the multiple in equity markets. Also, the low interest rate environment is another reason that should not be underestimated.

Please note central banks will provide accommodation for a considerable for the foreseeable future. In fact, the Fed has said that the economy needs accommodation for a considerable period, even with inflation above 2%. This is something the Fed has repeated many times, and thus we find it difficult to see a scenario where markets crash or correct considerably as they did in the beginning of the pandemic.

Irrespective of inflation, interest rates should remain low because central banks have unlimited firepower to keep them close to zero. As such our base case for interest rates is that they will remain at current levels for many years. In fact, this has been my base case for over a decade.

But market participants are conditioned to react to higher inflation. Their reaction, is usually, to sell equities preparing to move into bonds thinking rates will go up. But since interest rates will remain low, it is doubtful is if we see an exodos from equities to hide in bonds. Not only is there no yield anywhere to be found, but you can get a better yield in equities. So, it is difficult to fathom any kind of exit from equities, no matter what the inflation outcome is in the future.

So, while inflation is possible, central banks have the tools to keep interest rates at bay. A byproduct of such a policy is more liquidity in the economy and markets.

Will 2021 turn out to be a sell the news event?

So, will 2021 be a correction? Will market participants sell the COVID19 vaccine? We don’t know, but even if the market tries to correct, the additional liquidity from central banks will probably prevent such an outcome. However, the truth is that we don’t know what will happen, especially since valuations are so rich.

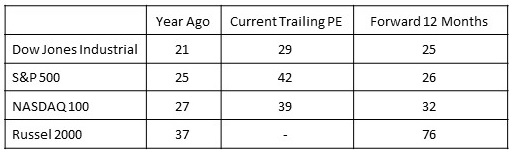

Sources: Birinyi Associates; Dow Jones Market Data

As you can see in the table above, the trailing PE ratio of the S&P is 42. Granted this is a high number because of depressed earnings due to the pandemic, however if we look at forward 12-month estimates, they are higher than the multiple pre-COVID. In the case of the Russel 2000, the multiple is almost double that of last year.

These valuations are very hard to swallow, even for those who justify a higher multiple because of the liquidity created by central banks. So, earnings have to increase by a lot in 2021 to reach last year’s multiples. But there are many uncertainties to such a scenario.

So, our base case for 2021 is that markets at best, will remain flat. And even if markets do go up, it will most likely be in the single digits at best. Valuation headwinds will probably prevent markets from continuing to expand the multiple, as has been the case over the past several years.

The Dollar is losing ground against most currencies, which is a good thing

As we have noted in the past, a weak dollar is good for the global economy and is supportive for global growth, especially for EM economies. A lower dollar helps companies and countries service their dollar debts, but also helps consumers around the world purchase iPhones. Historically, a lower dollar has been associated with a risk-on trade and better market returns. So, to the extent the dollar continues to drift lower, this should help support the global economy.

While we have no target for the EURUSD pair or the dollar Index, we are modeling a lower dollar for 2021. However, we do not expect the kind of moves we witnessed in 2020. The move from 1.08 to 1.22 in the EURUSD pair has not happened for over a decade. If the dollar continues to drift lower as we think, the rate of decline will be at a much slower pace than in 2020.

Will the rotation trade continue? Anecdotal evidence suggest it should.

As you have probably noticed, there is a lot of talk about an ongoing rotation trade. In other words, selling high momentum growth stocks and buying stocks that have a lower multiple or cyclical plays.

The chart above depicts the ISHARES 1000 value ETF (IWD) vs the ISHARES 1000 growth ETF (IWF). As you can see, growth did not always outpace value. After the crash in 2000, value was a far better choice than growth. And while after 2007 growth has done better, that will not always be the case.

The main reason why we are currently favoring value, is because of the extreme valuation of growth stocks. Simply put, most stocks that I come across are simply not investable due to valuation concerns. So, if we assume a rotation trade is happening (or will happen), this can last for years, not days or weeks.

Economies will continue to struggle despite a vaccine rollout

A double-dip recession is possible despite a vaccine rollout. Things are not great at the moment, and we do not anticipate a return to normality for at least 18 more months.

We are expecting many companies to become insolvent, despite fiscal help. Unfortunately, all the liquidity in the world cannot make up for lost business, especially if a company is leveraged.

Small businesses in many countries are in very bad shape, and it is doubtful most will make a comeback.

While everyone agrees that banks in this crisis are better off than during the 2008 crisis, nevertheless, there are still many unknows insofar the future quality of bank balance sheets, especially in Europe.

Solvency is still a problem

Remember, liquidity is not a substitute for a problematic balance sheet. This applies to both corporates and sovereigns, but also to individuals. While the solvency problem of the average consumer has been well managed in the US with the PPP program, the same cannot be said about Europe or the EM space.

In addition, many sectors like hospitality are permanently damaged. Many companies like airlines still need massive capital increases to stay solvent. Many other companies in the hospitality space will probably stay closed forever.

Central banks all over the world are pushing for fiscal help from governments. The US government alone will probably spend over $1 trillion in 2021. While the US government has the means to provide this assistance, most governments around the world can’t. This is especially true of countries in Africa.

What to expect in 2021

We do not expect equity markets to rally like they did in 2020. At best we think equities will be up in the single digits (if at all). The main reason being valuation headwinds.

Inflation should continue to remain low, and interest rates should remain at current levels or lower.

We do not think the dollar will be a safe haven in 2021. On the one hand the Euro is currently in style, and if inflation does resurface in the US, ultra-low interest rates will probably deter dollar investment flows, even in a risk off scenario.

While volatility is off its high, it is still stubbornly high and refuses to fall. The resurgence of COVID cases in many countries and the fear of a double dip recession is likely to keep volatility elevated during 2021.

While the popularity of passive ETF investing has been popular for many years, investors will actually have to do the work and pick individual names in 2021 if they want to make money.

The EM space will outperform western markets, and Europe will probably outperform the US.

About one third of sovereign bonds are in negative territory. This will likely increase in 2021.

With the Festive Season upon us, and holiday kindness being soiled not only in our personal lives but also in the business environment, as a part of giving back to our community and supporting those in need, Exclusive Capital has made a donation to the families in Cyprus. Our team has reached out to the families who during these challenging times may not be so fortunate and provided custom-made gift baskets with included food and clothing vouchers.

Taking a step back from the everyday hustle and putting a joint effort to create and share the holiday spirit has been a truly rewarding and positive experience for all those involved, as we believe that the true joy of the holidays comes from giving back, supporting causes that matter and sharing that touch of holiday magic.

Wishing a bright and peaceful holiday season and a prosperous New Year from Exclusive Capital’s team and management.

As we are leaving behind a volatile year in the financial markets, we expect that the current uptrend price momentum in the commodity sector will continue throughout most of 2021.

We remain optimistic about the overall commodity market picture for the next year and we see another 10%-20% upside from the current price levels as the global economy comes back online, and “cyclical” sectors will benefit from a post-pandemic reopening.

The broader rally in the growth-led commodity sectors such as energies and industrial metals could be supported from the global economic growth after the pandemic, driven by an effective rollout of Covid-19 vaccines around the world, the continued fiscal and monetary relief stimulus to help stem market collapse, and the rebound in the global manufacturing and construction activity.

The vaccination of at least 50% of the global population until May 2021, could help bring a conclusion to the deadly pandemic and reopen the global economy, increasing the demand for commodity products not only in Asia but also in Europe and North America for manufacturing and construction usage.

China, as the world’s biggest commodity consumer (50% of the global demand), was the first country that exited from the Covid-19 crisis and this helped them recover quicker than the rest of the world. The country will see its economic growth rates rebounding above pre-pandemic levels in 2021 amid the low rate of virus cases in the country and the unprecedented infrastructure stimulus from the Chinese government, benefiting the commodity sectors.

The commodity market witnessed a roller-coaster ride in 2020

What goes up must come down and then usually goes back up again, at least in the case of the commodity prices in 2020.

The COVID-19 pandemic has plunged the global economy into its deepest recession since World War II, causing huge losses (more than 50%) in the prices of the commodities. The sector experienced the worst demand shock (-30% y-y) in their history amid the impact on their demand from the social lockdowns to contain the spread of the virus.

However, the commodity prices have since rebounded with surprising strength, recovering all the pandemic-led damages, even as Covid-19 cases continue to soar in Europe and the USA.

Industrial Metals: Bullish outlook for 2021

Forecasts:

12-month forecast for Copper prices to average near $4 per pound, up 10% from the current levels.

It is highly probable that the prices of Copper will retest the existing record highs of $4.60 in the period Q4 2021-Q1 2022. In the case of a stronger-than-expected global economic recovery, it may rise 30% from its current levels.

We believe that the industrial metals will continue their reopening-led rally into 2021 amid the hopes for a vaccine-related global economic recovery, the robust industrial demand from China, and the massive “green” investments.

The prices of the base metals showed impressive resilience to the pandemic, outperforming everybody’s expectations during the second half of 2020, and rising above their pre-pandemic levels. Copper prices climbed at $3.60 per pound at mid-December, hitting their highest since 2013, the Aluminium prices surpassed the psychological level of $2.000 per tonne, while Iron ore has been on a stellar run amid robust Chinese demand and supply concerns over the recent trade tension between China and Australia (possible tariffs on iron ore exports).

“Doctor” Copper is widely traded as a proxy for global economic health since its demand depends on the global growth rates and the construction-industrial activity. The usage of Copper and Aluminium in automobiles and constructions has taken off in the last decade, thanks to their good conduct of electricity, recyclability, and lightweight.

Industrial metals could also benefit from climate technology developments in 2021. Politicians including the European Union leaders and the new President of the USA Joe Baiden have promised massive “green” investments to expand the renewable energy capacity and to reduce carbon emissions. Copper and Aluminium will see their demand skyrocket since they are key elements to some climate technologies such as electric vehicles and their batteries, wind turbines, and solar panels.

Finally, the growing supply risks could act as a major bullish price driver in 2021, as a structural underinvestment in copper mines is seen in the last decade, caused by the low prices and lack of cheap liquidity amid the financial recession. The supply risk could deteriorate if we combine the low Copper stockpiles around the world and the frequent supply disruptions from major mines in Chile and South America amid labor strikes.

Crude oil: Bullish outlook for 2021

Forecasts:

12-month forecast for WTI and Brent crude oil prices to trade between $50-$55 and $55-$60 per barrel respectively, up by 10%-15% from the current levels.

It is highly probable the WTI and Brent crude oil prices to retest the pre-pandemic levels of $60 and $70 per barrel respectively at the Q4 2021-Q1 2022 in case of geopolitical risk premium, up 25% from the current levels.

We believe that the crude oil prices will continue their upward momentum into 2021. Brent crude oil price moved back above $50 per barrel in mid-December 2020, for the first time since the start of the pandemic, while the WTI crude climbed at $48 per barrel, recovering most of their pandemic-led losses in Q2.

The demand and supply dynamics in the energy markets will play a significant role for the crude oil prices next year. The bullish price outlook will be supported by a limited increase in crude oil supply from OPEC and its allies led by Russia, and by the growing optimism that the start of the COVID-19 vaccine rollout will drive a recovery in the global fuel demand in 2021.

Energy prices will also benefit from the rebound in the economic activity in China and other Asian industrial countries after the pandemic, which consumes in total more than 30% of the global oil supply.

The progress with the mass Covid-19 vaccinations in 2021 will be a bullish event for oil prices as it will put the global economy on a path to sustained recovery, affecting the oil demand in the second half of next year.

With vaccines on the horizon, we expect a significant rebound in the travel and transportation activity around the world which has been restricted due the virus outbreak. People will resume traveling with planes, ships, cars, and trains for business and entertainment in the second half of 2021 propelling a robust recovery in the demand for jet, maritime, and gasoline fuels.

A weaker US dollar will be another positive catalyst for oil prices in 2021, as it is the de-facto currency accepted for global trade (most contracts priced in US dollars). The greenback has slipped to 2.5-year lows against most currencies (DXY-dollar index fell below 90), making the dollar-denominated petroleum products more attractive to energy importers with foreign currencies.

OPEC and its de-facto leader Saudi Arabia are major influencers for oil prices as they always manage to avoid large surpluses or deficits in the oil market. Therefore, the willingness of Saudi Arabia and its non-OPEC allies (led by Russia) to keep their crude production at low levels amid the higher supply from Libya and US shale producers and until the full recovery of the global demand in 2021-2022, will be another bullish catalyst for the oil prices in the long term.

The coronavirus-driven oil price crash combined with the market shift towards renewable energy investments, had forced the shale oil drilling companies to cut production and delay investments in offshore projects, creating the risk for a supply deficit in the long run, which is certainly bullish for energy prices.

On the negative side, we expect that the current rise of Covid-19 infections will continue damaging global demand growth. With virus cases surging to record highs across Europe and the USA, they have announced new lockdowns and travel restrictions to curb the spread, weighing on near-term gasoline and jet fuel consumption.

Bottom Line:

We believe that the current vaccine-led rally in the commodity sector will be the first leg of a structural bull market amid their improved fundamentals. Therefore, we expect the prices of the energies and industrial metals to go higher by another 10%-20% in 2021 from their current levels, while every price correction will become a buying opportunity for the investors.

RISK WARNING: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 66.67% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.Become a Client